A report issued yesterday documents the growing market for “justice tech” — startups focused on reducing inequities in the criminal and civil justice systems — and urges venture capitalists to invest in these startups.

The justice tech market has grown significantly over the past decade, the report finds, and investors have put over $77 million in more than 100 early-stage startups working at the intersection of tech and justice.

Even so, overall investment in justice tech has been limited. While over 200 VC firms have made one-off early-stage investments in justice tech, the investment landscape is fragmented, and 92% of investors in the market have just one justice tech company in their portfolio.

“Rather than redirect philanthropic dollars from policy and service organizations, there is an opportunity for venture capital investors — both impact and traditional alike — to coalesce around justice tech as an important area to support historically excluded and overlooked people in the U.S. and as an area of promising return on investment built upon scalable technology,” the report urges.

The report, Justice Tech for All: How Technology Can Ethically Disrupt the US Justice System, was published by two VC firms that focus on impact investing: Village Capital and the American Family Insurance Institute for Corporate and Social Impact (AmFam Institute).

It grew out of a summit on justice tech convened in September 2020 to discuss ways to move forward in redefining criminal and civil justice tech from an ethical, human-centered perspective.

Tech-Enabled Innovation

The report provides two definitions of justice tech. The main body of the report defines it this way:

“Justice tech in the US refers to technology-enabled innovation that supports people affected by the US criminal and civil justice system and their families (and the organizations that serve them) – from initial interception by law enforcement to incarceration to reentry.”

But the introduction provides a slightly different definition that is described as the way most impact investors mean it:

“Startups that are built with the goals of reducing inequities in criminal or civil justice and creating opportunities for justice-involved people.”

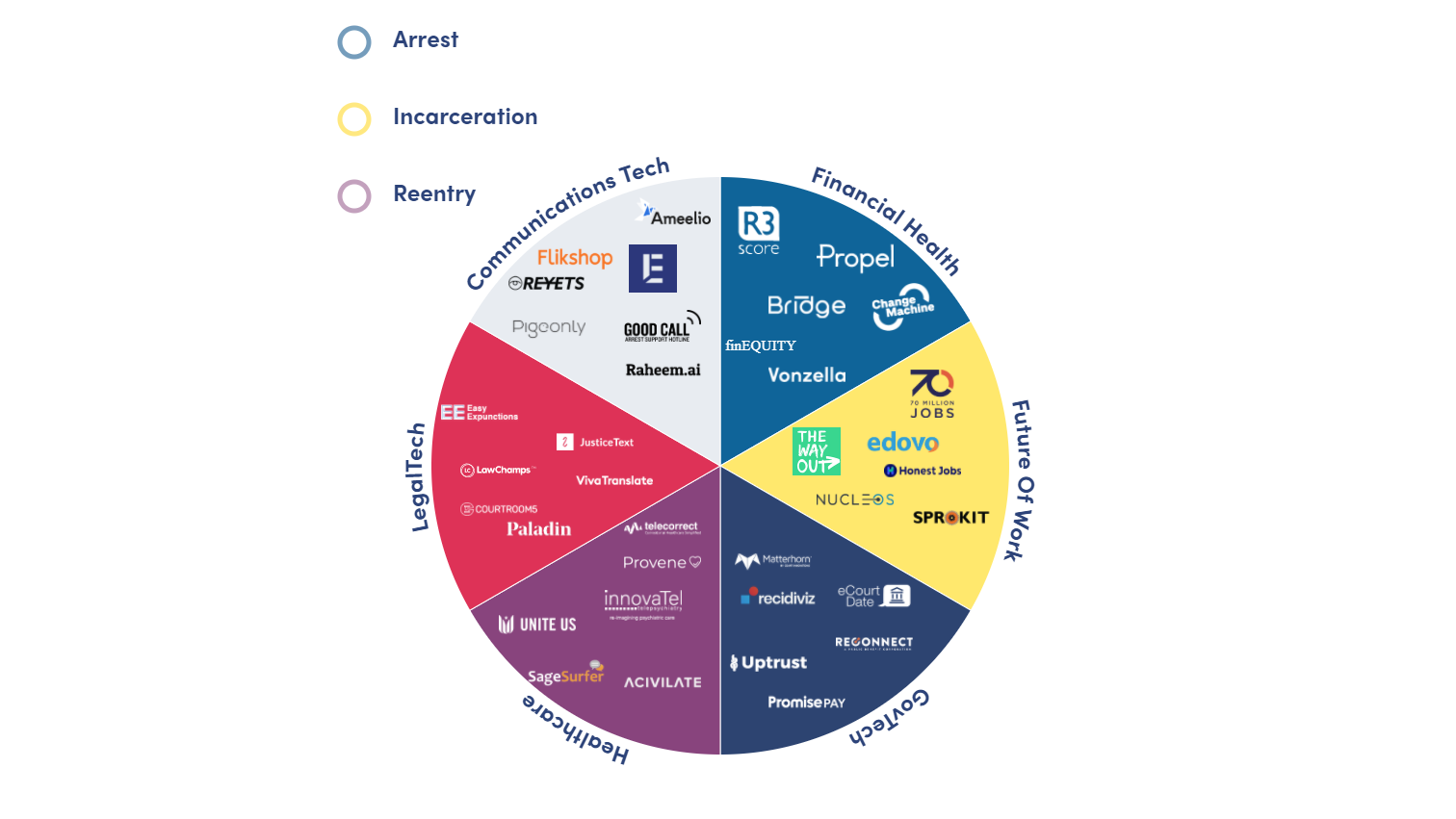

Six Key Verticals

The report maps the justice tech ecosystem.

Either way, the report maps a broad landscape of justice tech that goes beyond legal tech into finance, healthcare, government and communications. It defines six verticals related to justice tech:

- Financial Health. Technology that helps justice system-involved people and their families achieve financial security and stability and the ability to thrive. Examples of startups in this vertical are Vonzella, which provides cost-sharing services to offer bail insurance for defendants, and finEQUITY, which provides financial services for incarcerated individuals.

- Future of Work. Technology that expands access to education and employment for justice system-involved people. Startup examples include Edovo, a provider of digital educational and rehabilitative services for incarcerated individuals, and 70 Million Jobs, a platform to connect formerly incarcerated people with career opportunities.

- GovTech. Technology that makes government systems (like the courts) more accessible or efficient. Startup examples include eCourtDate, a messaging, scheduling and analytics platform for courts, and Recidiviz, a nonprofit platform to power data-driven interventions in criminal justice.

- Healthcare. Technology that supports the mental and physical health of currently and formerly incarcerated people. Startup examples include telecorrect, software to help lower the cost of correctional medical and mental health services, and Acivilate, a compliance platform to connect justice agencies and human service providers with returning citizens to reduce recidivism.

- LegalTech. Technology that expands access to both civil legal resources and criminal legal representation after arrest. Startup examples here include CourtBuddy (now LawChamps), which helps consumers connect with local attorneys, and Paladin, a platform that connects attorneys with pro bono opportunities.

- Communications Technology. Technology that helps just system-involved people stay connected with family, friends and service. Startup examples include Raheem.ai, a platform for reporting police conduct, and Pigeonly, a platform that helps inmates connect with their loved ones.

For each of these verticals, the report provides an overview of the market and analysis of the opportunity for investors and entrepreneurs. It then turns to an overview of justice tech funding, listing some of the active investors and the companies in their portfolios.

It finds that a lack of investment capital has hindered development of for-profit startups in this market. While grant-making foundations have deployed billions of dollars to advocacy and direct-service programs, they have reluctant to put money into for-profit entities, leaving entrepreneurs strapped for cash.

Recommendations for Investors and Entrepreneurs

To help investors evaluate opportunities in this market, the report offers what it describes as an early beta version of a “justice lens investing” framework that identifies the questions to ask:

- Team. Does the team include justice-involved people, either at the founder or employee levels?

- Value proposition. Is the value proposition of the product providing meaningful improvement to the lives of justice-involved individuals and/or their families?

- Product. Is the product designed with the collaboration or advice of justice-involved people

- Business model. Does the company’s business model exploit inefficiencies in the system rather than lay the cost burden on justice-involved individuals and their families?

- Scale. Is the company’s success tied to the reduction (rather than the expansion) in the number of justice-involved individuals?

- Exit. How do the company’s investors and exit opportunities affect justice-involved people?

The report concludes with a series of recommendations aimed at entrepreneurs, investors and limited partners, and corporate leaders.

For entrepreneurs, the report’s recommendations focus on integrating the voices of justice-involved individuals and groups early in the decision-making process, building relationships with an array of organizations focused on supporting diverse founders, and building relationships with early-stage investors who have a deep understanding of the justice tech market.

For investors, the report’s recommendations boil down to “Just do it.”

“Now is the time to support and invest in entrepreneurs who are creating opportunities for people impacted by the criminal and civil justice system,” the report urges.