Clio has officially launched Clio Capital, a financing program designed exclusively for law firms that use the company’s practice management platform.

The product, which went live Feb. 26, provides eligible law firms with pre-qualified access to working capital through a streamlined application process directly within the Clio platform, bypassing the paperwork-heavy, rejection-prone process that has historically made borrowing difficult for small legal practices.

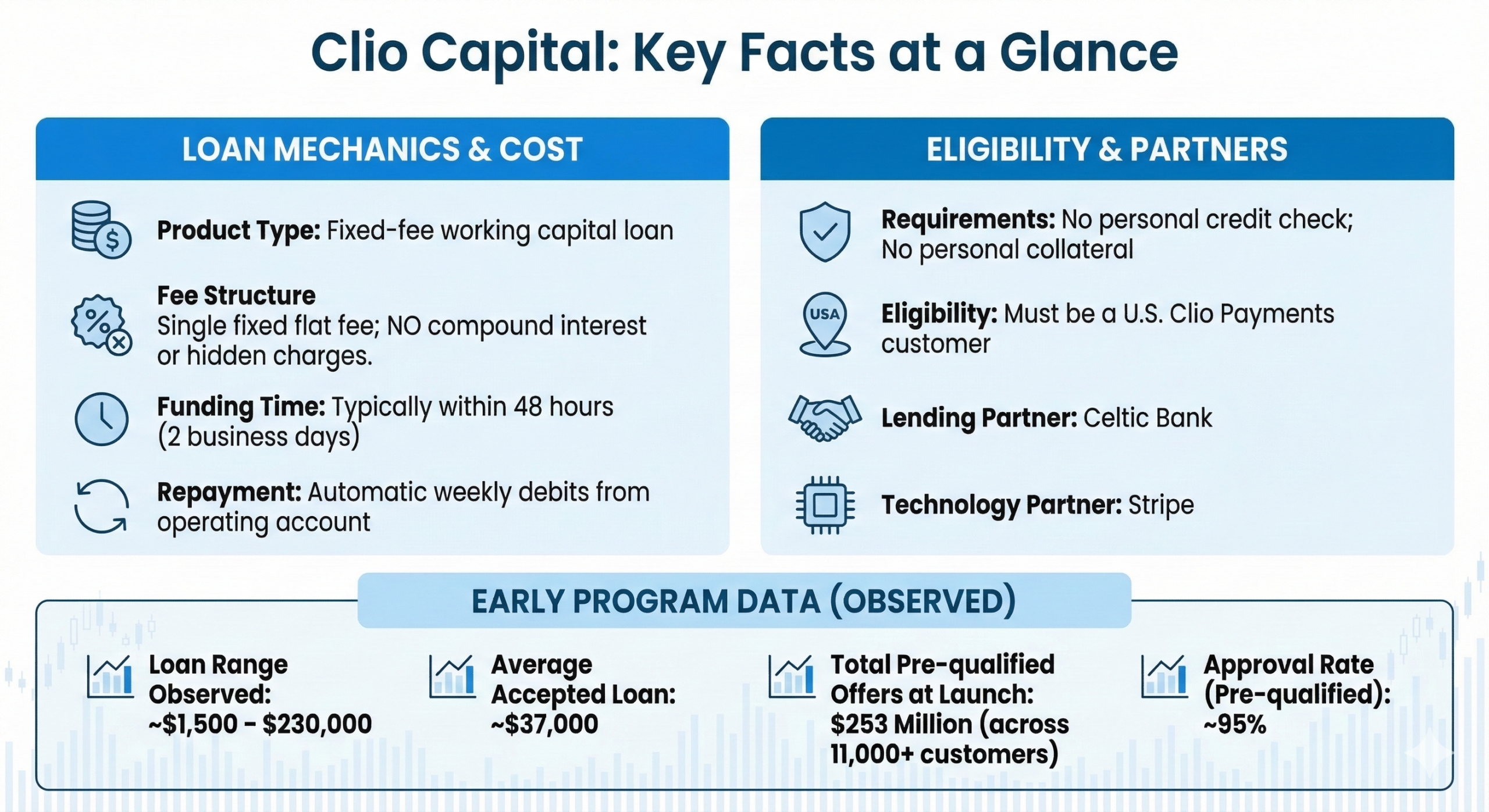

In an interview with LawSites, A.J. Axelrod, Clio’s vice president of payments and financial services, said the program had disbursed well over $1 million in loans within its first week of full operation, with more than 35 loans issued ranging from $1,500 at the low end to approximately $218,000–$230,000 at the high end. While still in its early days, the program’s average accepted loan amount so far is approximately $37,000.

In total, as of launch, roughly $253 million in pre-qualified offers had been extended across more than 11,000 Clio customers — though not all of those customers are expected to accept.

Clio Capital loans are issued by Celtic Bank and powered by Stripe. The program is available now to eligible Clio Payments customers in the United States.

A Market Underserved by Traditional Lenders

Axelrod said the motivation for Clio Capital was the structural market failure that has affected small businesses — including small law firms — for decades. The traditional loan process is time-consuming, manual and often discouraging, requiring applicants to gather financial documents, visit a bank, complete extensive applications, and frequently face rejection even after all that.

Beyond the friction, Axelrod said, banks generally have little economic incentive to lend small amounts. As a result, firms that need $1,500 or $5,000 may be entirely shut out of the traditional lending market — and may instead resort to carrying revolving credit card balances at interest rates of 20–24% or higher.

Law firms also face a challenge specific to their industry. They typically lack the tangible assets — equipment, inventory, real estate — that traditional lenders use as collateral. Recent regulatory changes to SBA lending rules have intensified these pressures, sometimes forcing partners to pledge personal assets such as their homes to secure business funding.

The time burden also falls disproportionately on lawyers. Every hour spent packaging financials for a bank loan is an hour not spent serving clients and generating revenue. For many small firm owners, the calculus simply does not favor pursuing a traditional loan.

Pre-Qualification Based on Payments Data

What is particularly interesting about Clio Capital is that it uses data that Clio already has about its customers to underwrite loans prospectively rather than reactively.

Because Clio, through its Clio Payments produce, processes payments for tens of thousands of law firms, it has real-time visibility into billing frequency, payment volumes and related financial activity. Clio Capital uses that data for a pre-qualification process that evaluates all eligible Clio Payments customers on a rolling basis.

Firms that meet eligibility criteria receive a pre-qualified offer directly within Clio Manage, the company’s practice management application. The offer includes a loan amount and interest rate, and firms can use a slider to adjust the amount they want to borrow.

Because customers are pre-qualified before they initiate an application, Clio projects an approximately 95% approval rate — meaning only about 1 in 20 customers who click through to accept an offer will be declined.

A secondary layer of underwriting supplements the payments data, Axelrod said. Prospective borrowers are asked to connect their bank account (with their consent) so that additional signals can be reviewed, such as whether the firm has an active bankruptcy or a pattern of returned payments.

Axelrod described this step as designed to be as frictionless as possible, and said it accounts for most of the cases in which pre-qualified customers are ultimately not approved.

Completing the application typically takes only a few minutes. The application then enters a brief review queue — usually resolved within a day — after which funds are transferred via ACH. Clio says most borrowers receive funds in their bank accounts within approximately 48 hours.

That pre-qualification process means that eligibility is based on a firm’s business performance within the Clio ecosystem — not on the personal credit scores of the firm’s partners. Borrowers do not need to pledge personal assets as collateral.

Loan Structure and Pricing

Clio Capital loans are structured as traditional installment loans, meaning they have a fixed repayment schedule with a defined term and a fixed total cost. There is no compound interest, and Clio says there are no origination fees, data processing fees or other add-on charges.

Axelrod said the effective interest rate Clio has been seeing runs around 15%, which he described as meaningfully better than typical credit card rates (roughly 22–24%) and competitive with what a borrower might expect from a quality small-business loan.

He noted that some alternative lenders charge rates of 30–40% or obscure their true cost with fees, neither of which applies to Clio Capital.

Each borrower’s offer is customized based on their individual payment history and risk profile, so rates and available loan amounts will vary.

Repayment is handled through automatic weekly debits from the borrower’s bank account, which Clio describes as designed to keep cash flow predictable without requiring manual management.

If borrowers run into difficulty making repayments, Axelrod said, Clio intends to work with them, potentially through payment relief or program modifications, rather than leaving them on their own to navigate the situation.

Partnering with Celtic Bank and Stripe

Clio is not itself a lender, bank or licensed depository institution, and it does not hold the loans on its balance sheet. Instead, the program operates through a partnership structure that Axelrod described as drawing on the respective strengths of each participant.

Clio contributes what Axelrod characterized as its two most valuable assets for a lending program: distribution (direct access to a large, engaged base of law firm customers) and data (detailed, real-time payment and billing information that can be used to underwrite credit decisions).

Celtic Bank, a Utah-chartered industrial bank, provides the regulatory standing and cost of capital required to issue loans at competitive rates. Stripe serves as the payments infrastructure underpinning the program.

Axelrod noted that navigating the regulatory landscape for lending — which involves both federal rules and state-by-state licensing requirements — is a significant undertaking that Clio could not efficiently manage on its own.

The bank partnership allows Clio to offer a compliant product without having to build that regulatory infrastructure internally.

Privacy and Data Use

Addressing potential privacy concerns, Axelrod said that Clio discloses throughout the application process exactly how customer data can and cannot be used.

The program operates under what he described as a data wrapper, meaning that the payments data and lending/repayment information collected as part of the program can only be used for purposes within that program and cannot be repurposed elsewhere within Clio’s platform or operations.

For example, if a borrower misses payments on a Clio Capital loan, Clio cannot use that information to affect the customer’s standing with respect to other Clio products.

Axelrod said Clio takes compliance across all dimensions of the program, not just privacy, “incredibly seriously,” and he said that the company chose best-in-class partners in part because of their compliance capabilities.

Who Is Eligible

Currently, eligibility for Clio Capital requires that a law firm be an active Clio Payments customer. Payment processing data is what drives the pre-qualification engine, so firms that do not use Clio Payments do not yet qualify.

Axelrod said Clio hopes to expand eligibility in the future by incorporating additional data sources, so that firms using Clio for practice management but not payments might eventually qualify.

He noted that the program is starting with payments data because that data provides a high-confidence, real-time signal about business health that enables favorable underwriting terms.

The program is currently available only in the United States. Axelrod said the company intends to explore international expansion, but emphasized that regulatory complexity makes it important not to rush into markets without the right partners in place.

How Firms Can Use the Funds

Clio does not restrict how borrowers use their loan proceeds. The application does not require firms to state a specific use of funds, and a firm’s stated purpose does not affect whether it is approved.

The early signals suggest a broad range of uses, Axelrod said. Cash flow management is a common motivation — small firms with irregular revenue still face predictable obligations such as payroll, rent and operating expenses.

Beyond that, firms are using capital to invest in growth: new technology, marketing, hiring and other initiatives that require upfront spending.

Axelrod also foresees that data on what types of firms apply for loans and how they use them could eventually yield meaningful industry-level insights.

Axelrod also foresees a possible positive feedback loop in the program’s design. He expects that borrowers who successfully repay a loan will be quickly re-approved for new financing — and potentially eligible for larger amounts at lower rates. Successful repayment is a strong credit signal, and Clio intends to use it to offer progressively better terms to reliable borrowers.

The goal, as he described it, is to create a cycle in which firms that gain access to capital, deploy it effectively, grow their practice, and repay their loans are progressively rewarded with cheaper, more accessible financing.

Broader Fintech Expansion

Clio Capital is not the company’s first foray into financial services. The company already offers Clio Payments, a payment processing product, as well as a buy-now, pay-later feature for legal services. Axelrod said that Clio Capital represents an expansion of that broader fintech strategy, and that additional financial products are under consideration.

He noted that different firms have different financing needs. A revolving line of credit, a multi-draw facility, or a merchant cash advance might serve some customers better than an installment loan. Clio intends to listen to customer signals and develop products accordingly. The current installment loan was chosen as a starting point because it is simple, transparent and broadly applicable.